“The negative outlook on Wahoo reflects the ongoing operational hurdles related to weaker than expected demand, intense price competition, and increasing cost pressures. If the company’s cash flow and liquidity position deteriorate further in 2022, it could add significant uncertainty to its ability to maintain a sustainable capital structure.”

Looks like Wahoo is in for a bumpy ride, but others in the fitness sector will likely be hit also (don’t know their cash structure). Fairly evident that the sector has run at an unsustainable level during the pandemic. Also explains why Zwift pulled out (or paused) their work on hardware.

I think that the used/preowned market is something that they did not account for as well. I buy all my cycling toys used and just got a used trainer (Tacx Neo) to replace my KCKR gen 1 (which i also got used and is for sale, if anyone is in the market). I got my bolt and elemnt used as well.

Top that off with Wahoo selling reconditioned units and a flood of people selling Peloton bikes and you have a perfect storm.

I hope TR weathers the storm well.

It started with a large discount on the the Kickr trainer weeks ago (listed in the Deals thread). Elemnt head units have had a cash back rebate for a while too and it’s still active. The latest Rival discount is actually the 3rd step they’ve used. So there have been moves in play for several weeks on several products. This may persist until they can get whatever over-stock they have to a more manageable level.

as far as I can tell, many businesses take the attitude of “get while the gettin’s good” with little insight or thought that good times don’t last forever.

its marginally comical to me how companies this size can be so short sided. I realize we’ve never had anything like covid to make predictions based off, but theres no way any CFO worth their pay could have predicted pandemic level sales would be sustainable long term. Peloton CFO openly said “we didnt expect people to go back to the gym” when they reported their massive loss.

As for the watch, like it or not, apple owns the sector, followed by garmin. wahoo is such a small player in the overall market.

To be fair I think most people use the apple watch as a regular watch with some fitness stuff but not geared like Garmin. Yes Apple sells more but the target demographic is not the same.

I agree, but what I meant was I don’t see many people cross shopping Apple and wahoo watches

Apple Watch has everyone from “I’m too lazy to reach in my pocket” to athletes

Garmin has a massive stronghold on sports but probably makes more money on their avionics.

Wahoo has the cyclists and runners that wanted to try something different than garmin

I made the same argument in the thread about the new Stages Dash. Cool product but doesn’t do anything garmin and wahoo units don’t already do and costs the same.

When I was running marathons, I’d always choose my Garmin over my Apple watch for tracking. But the Apple watch is so far ahead in everything else that I’d usually just wear the Apple watch all the time and put the Garmin on my other wrist for runs. Now that I don’t run anymore, the Garmin sits in my nightstand. I did try the Venu 2 as an Apple replacement but it was missing too many features I have grown to love. The Wahoo watch wasn’t even my radar. Maybe if I was in the Wahoo environment with a head unit.

Plus honestly feels like there isn’t much in the way of new features in the last ~5 years to drive people to upgrade/replace trainers. Smart trainers and direct drive trainers were a big leap over what we had before and a very compelling reason to upgrade at an relatively affordable £500-1000 that opened up the worlds of interval training in erg mode, Zwift, etc. Improvements since then have been pretty marginal/niche and much less compelling IMHO. Incremental improvements in noise and accuracy. New features like steering, road feel, tilting for slopes, headwind fans, all of which for me lie somewhere between “nice to have” and “unnecessary gimmick”. And smart bikes at prices in the £2-3000 bracket which still buys really quite a nice real bike that I can ride indoors and out!

Seems to be that all companies have a short term view, probably driven by the need to keep shareholders happy and the nature of their bonuses, to maximise growth quarter to quarter. Nobody wants to think long term because all the incentives are short term. End result: A warehouse full of stuff they can’t sell because they didn’t look past their current bonus period.

Tech/growth companies like PTON think that if 5-10% of the population sign up for their service, they’ll be so rich that they won’t know what to do with the money.

Companies like Wahoo and Garmin are much more established and should be able to project sales a little bit better. What was Wahoo going to do, not try to produce more trainers during the pandemic?

None of these companies probably plan for a recession where people really tighten their belts and buy nothing extra at all. That’s going to happen next.

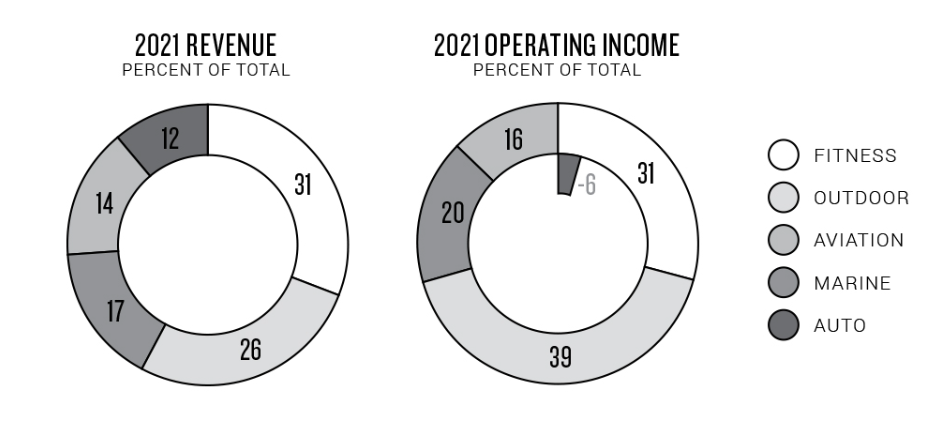

Garmin’s segment reporting indicates the opposite. In terms of operating income absolute value, aviation is the second lowest segment, after auto. Marine, outdoor and fitness are each significantly higher, with outdoor more than twice as big as aviation.

Garmin has also suffered from the rebound effect - their Fitness segment shows 28% y/y revenue decline for Q1 2022, and 99% operating income reduction. Overall however, they are still growing (9% top line), albeit a a lower level of profit (8% reduction in operating income). Outdoor saved their skin, with 50% revenue growth and 62% operating income increase. The segment represented 33% of revenues, but 65% of operating income in Q1.

Aviation took a beating in 2020 (go figure), but even before that, the Fitness and Outdoor segments have been the strong drivers at Garmin. And the Auto segment has been a boat anchor for years .

Agreed. Humorously, I’d say that adding something as “old skool” as a wired connectivity option - paired with app support - would be a reason for a lot of people to upgrade. Other than that, I honestly have little reason to upgrade from my Kickr Core that I bought on sale three years ago.