And apparently, it’s a ship that “heals”. (“The ship was healing sharply to starboard, …”)

Ok, I’ll crawl back under my rock.

And apparently, it’s a ship that “heals”. (“The ship was healing sharply to starboard, …”)

Ok, I’ll crawl back under my rock.

Well, “listing” is probably the more accurate phrase. “Heeling” is usually associated with tipping due to wind, not taking on water.

Your pendantic friend, P13.

![]()

Difference is that with the 13.00 a month there is no power stats. That is the biggest difference. Without power you are not on the leader board as well.

I don’t know that unsold “bikes” at Walmart is a true reflection of the availability of bikes across most major brands. In North Carolina here in the USA, local bikes shops continue to have issues getting stock. Bad part is these dealers must commit to X number of bike in order to get special pricing or first pick on certain models as they become available. Then these manufactures are not delivering on time or at all. One shop I know of had an estimate of 14 months on delivery of a road bike with a retail over 10K USDs. Not many buyers are going to wait that long. Another shop has sold brand X for over 40 years but can’t get product so they are having to pick up others lines so they can have product to sell.

As an owner of a Pelton, I don’t see anything or have not seen any increase in the subscription price. I have seen information on the cost of the bike and bike+ going back up. At the time we bought ours there was a big discount on the base model as the new Bike+ was released. Then around Christmas time they discounted the Bike+ as well. If anyone has information on the subscription cost going up please post or send me a message.

@Pbase posted the press release but the price increased about 15% in April 2022 ($39 to $44).

It just seems like a huge discrepancy in price for a little bit of functionality that probably doesn’t mean a lot of most people.

It was just another data point. More data points - I’ve seen bikes in stock at local bike shops which is a huge change from 1.5 years ago. $800 Trek mountain bikes in stock at my local dealer (was looking for my kid). That price point was unobtainable during the pandemic.

I also went to a high end bike shop recently - tons of $10K+ Bianchis, Colnagos, and others in stock. They are also a Specialized dealer and the Aethos was in stock. Tarmacs are still hard to come by for some reason. I’ve seen Emondas in stock (looking for myself).

I’ve seen Shimano 12 speed generally available now.

It definitely seems like supply is coming more in line with demand.

I agree with you, the price difference is huge…but really, there are 2 things people love about Peloton. First will always be the instructors and the feeling of community. Second is the leaderboard.

What’s sticky about Peloton for consumers is the feeling of belonging. Of feeling like they’re doing this with a group of friends and “people like me”. It’s motivating. Like anything else, people want desperately to “belong”. One of the key parts of this is seeing where you “rank” in the daily competition. Sure, there will always be strong people and weak people (and don’t even get me started on calibration), but even the slowest riders ride with other slow riders. They start to see names they recognize. They want to move up one place in the rankings. They don’t want to get passed. They even sprint during the cool down to improve placement. Then they join Facebook groups with those same people. They chat. They share their successes and failures. They join group rides together. They do meetups and fly from all over the country to ride and party together.

This is why Peloton hit a nerve and hit the stratosphere. With no power data and no leaderboard, you miss out on all that and it just becomes another workout engine.

100%. Former racer friends who no longer compete, and often just ride “the wife’s peloton” seven days a week, always claim they don’t pay attention to the power measurement. But somehow, they all know exactly what their Peloton Power ™ is, and always know exactly where they are on the leaderboard.

FWIW, whatever decisions the Peloton leadership made and may have missed on, things like Peloton and Tonal and some of the mirror type systems are always going to appeal. I’m still a stoic individual, rollers and barbell, stare at the basement wall and grind it out person. But completely understand the appeal of modern looking workout equipment, entertainment and a community to exercise with.

Stock down to ~$7

Here’s another recent article:

Brutal.

The 1.2b loss has been known for a while. The primary driver of stock hit is the same thing that hit Apple - fear of recession and its effect on consumer spending.

Motley’s analysis is pretty thin beyond its recession/ revenue comments. Are consumers really going to flock to competitors? Or not buy at all? Think: Apple situation.

Peloton still has an amazingly loyal customer base and even great new products. There is no #2 in the market. But they have a monster cost structure that is getting worse with current times. Their challenges are huge but its a very reasonable long term buy if one is interested. Just not sure its the bottom given the economic climate.

Comparing it to Apple isn’t exactly apples to apples!

Apple actually makes money, and have many sources of revenue stream. Is recognized as a market leader, is one of the most valued companies in the world etc.

Peloton has a very immediate and real problem, they’re losing members after the COVID surge, and it appears that they (new members) aren’t very excited about purchasing services and equipment for working out in your basement right now.

Is it inconceivable that customers might go to a competitor or not buy at all. If so, how come?

I don’t see the connection. Can you elaborate?

It appears that I wasn’t clear with the point(s) I was trying to make. So I’ll try to explain it differently . . .

Peloton does indeed have huge challenges created by an enormous operating cost structure. And these challenges (e.g. cash, mgmt turnover, etc.) are being exacerbated by the current (and worsening) economic climate.

There are certain companies, known as bell-weather companies, that the stock market looks to as signs of economic strength (or weakness), for consumer spending trends. Apple, Amazon, Target, Walmart, Home Depot, and Lowes are among them. When Apple announced earlier in the week iPhone 14 demand was substantially below expectations to the point that they are curtailing their new production facilities that became a major indicator to investors for weak consumer spending (and supports the fear of a recession).

The bottom line (of my line of thinking is this). Revenue slow down of Peloton is largely driven by consumer spending in a similar manner as it has affected Apple. In a similar manner that it is not likely that many customers will buy a lower cost smart phone (e.g. a knock off) to Apple because of the economy, I don’t believe there will be flocking to Peloton’s competitors as the economy slows. Rather I believe that, similar to Apple, consumers will hold off on [discretionary] purchasing all together.

I follow your line of thinking. However to Apple this would mean a decrease in their income is a bit less. When 2022 closes out Peloton will have had a negative net income for the 5th straight year. I’m no economist but I feel like that’s typically not a sign of a sustainability for a company.

The users they have are incredibly loyal (a result of the top notch experience they create for them), but they probably need to figure out how to balance their finances with what they’ve got and hope some big player comes in and buys they out as you can’t bleed billions forever. I wonder if they are making money on the rowers? I know some users who want to go out and buy them despite how much more it is than the gold standard (Concept2)

The impact to Apple as a company of the downturn in consuming spending is close in inconsequential.

For Peloton, it is huge, including questions of sustainability (as you point out), particularly given how tough of a position they are already in.

Yes! To put this in perspective, Peloton’s customer retention rate has been about 3x that of TrainerRoad.

Yes, the financial issues are their #1 challenge. And it’s not clear whether it will be banks that keep them afloat in the interim or a buyer.

The rowers are probably “making money” from a variable margin perspective. But it’s probably too small to meaningfully offset the company’s overall financial challenges yet.

As for Concept 2, to me it seems to be a similar situation to when the Peloton bike entered the market - premium experience for a premium price. Some will certainly pay for that. I think the larger product/market question for Peloton is whether they can go after the middle market without canabalizing their premium market.

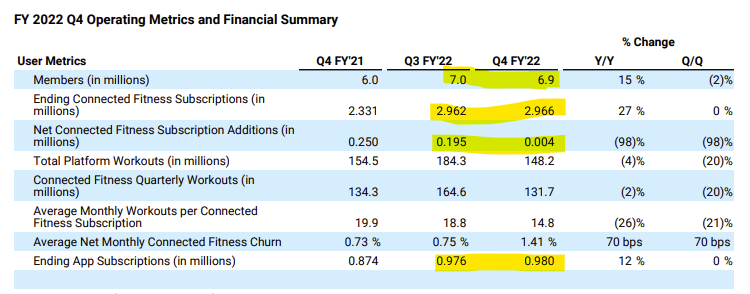

Not as of their latest earnings, they aren’t. Well, maybe they are - I think there’s actually either an error or a rounding error here. If they are losing, it’s a fraction of a percent, if they arne’t, it’s a fraction of a percent gain. Check out this chart. It actually doesn’t make sense. Peloton measures subs in both ‘Connected Fitness’ (meaning they bought Peloton hardware), and the App Subscription (like on an iPad or whatever). In both of those categories, as well as net additions, they went up. Yet somehow, the total went down.

In thinking about it, I think where it’s messy is that paying subscriptions went up (barely), but some non-paying family members canceled/deleted their accounts. For example, friends and family that have stayed at our house have created an account (for free) to use our Peloton Bike/Tread, yet, don’t pay otherwise. So at some point some of them deleted their accounts.

Either way, they’re not losing paying members, which is more or less all that matters in the context of are they losing paying people. They (net) gained a handful.

Funny. I was basing my comments on the same chart.

So – maybe I mis-read it. I see a slight decline in net membership. A slight up-tick in subscriptions ending. And app subscriptions ending. Churn is up slightly as well.

I’m also factoring in ample reporting suggesting that the market for bikes has gotten very, very soft. To the point that Peloton is considering adding a CPO or similar offering (per a recent NYT article).