So you’re telling me you remember Bowflex classes with “50 friends and having the teacher address you by name, play the song you requested, or crack a joke about when they met you in person. And that could happen every single day in a brand new class with brand new music, people, and workout structure”?

Because I don’t remember any of that. I remember a machine with a bunch of flexy arms and a dvd. That you did alone. With no interaction with others. The same dvd over and over.

If these companies are viewed as anything other than as fitness companies like gyms, yes. The whole idea that Peloton was anything other than a competitor to spin studios / gyms was laughable in my estimation.

This is a true statement to the extent that you believe that the size of the gym market and the size of Peloton is a zero-sum game (one goes up; the other goes down; and vice versa). It’s quite possible that mathematically it is true as the gym market has gotten crushed while, regardless of its stock fortunes and misfortunes, Peloton has acquired a huge customer base.

However, intuitively it is not because of the breadth of uses of the gym and similarly of Peloton. Peloton’s expansion into other areas, such as yoga and meditation and even stretching training isn’t something most gyms are particularly good at and many of its customers post the initial growth were not gym customers.

I think arguably the interesting thing about the Peloton ups and downs is simply that it’s public. Meaning, that if we look at most of the indoor training space, they’re not publically traded companies, and thus, we have no idea. So, it’s all supposedly roses.

Take Zwift for example, there seems to be an implied assumption in these threads that somehow Peloton is doing worse than Zwift in terms of growth. But the numbers that we see actually show, very clearly, the opposite. We have very public numbers on Peloton each quarter, and each quarter they grow. Revenue is complicated and grey - but that’s mostly their own doing. And share price is messy, but share price is a poor indicator of financial success (as evidenced a million different ways). Peloton’s share price is mostly down because of both own-goal stupidity and general human stupidity (like the Sex and the City mess).

So we know Peloton’s direct numbers, but we actually don’t have a certified Zwift (or TrainerRoad even) number of how things are going there. Instead, we use a proxy. In Zwift’s case we use concurrent users. and looking at that, things aren’t where we were a year ago. Last early January peak-Zwift was recorded at 43K, and I don’t see any record posted since then higher. Thus, here we are a year later, and basically growth is flat. The highest day’s we’ve seen are in the 41-42K range. Certainly, the particulars of a peak-Zwift date can be weather-driven, but if there was any meaningful growth there, then we’d have seen them bump against that or above that occasionally.

While stock market valuation has its limits on comparing companies, the name Bowflex (for example) has come up multiple times in this thread. Bowflex is part of the Nautilus family of companies. Just for a sense of comparative size, even at its depressed value of $8B, Peloton is 50x more valuable than the entire family of Nautilus companies ($160M).

As for TrainerRoad, as we all know it is a private company so Its #s are not publicly available. But I’ve done some estimating based on a few ofTR data points comparing it to Peloton, and roughly Peloton is between 2 and 3 orders of magnitude (100- 1,000 times) larger based on number of users and rides than TR.

The point is not that Bowflex, Nautilus, TrainerRoad (and others) aren’t great companies. It’s that Peloton is a real force in the indoor fitness industry and has done so by revolutionizing the indoor experience.

But a major difference here is that flat is not as harmful to a company like Zwift which depends on subscriptions as their primary source of revenue. For a company like Peloton, which is primarily dependent on hardware sales followed by subscriptions, when hardware sales start to decline, it can be more destructive, let alone when they start having to suspend production.

I persoanlly expect Zwift (and even TR, but to a lesser degree) to see declining membership moving forward. The growth was simply not sustainable.

Its pretty bad when you’re trying to attract more rounds of VC funding. If you’re showing no growth in revenue that won’t convince investors of your future viability…

@dcrainmaker The supply chain side of things has also dramatically impacted Peloton’s growth and user metrics. Their Instagram posts result in 100+ people every post saying “If only I had my Pelton bike I ordered 3 months ago” blah blah blah.

My wife hops on mid morning on Saturday with Alex Tousant brining 25k people to each of his live rides every ride. That’s just one of her favorite instructors, they all have huge followings. My wife used her Bike+ 180hours last year, and I think she’s middle road maybe dead average user for active time in the system.

This is a HUGE issue for Zwift. In addition to it being the key metric for of growth (followed by stickiness), it is one of the key metrics of how they will be valued, whether the path is going public or acquisition.

I didn’t say it wasn’t an issue, I said it was not as harmful. They don’t have millions of dollars of inventory sitting around, aren’t subject to higher decreases in revenue, etc.

@Power13 are you sure ? I’d like to read or see something supporting that claim. Anecdotal as it is I know people who waited months. We ordered within the first 5 hours when the Bike+ came out, it arrived the next week and then other locals in my area waited months and we are in NYC metro the Pelton homebase.

I get trolling, but nearly every sector has had major supply chain disruption and delays.

That could be the difference…I was referring to the base model. Not only have they had inventory for months, they have been discounting them to try and move them. You don’t discount something you don’t have in stock!

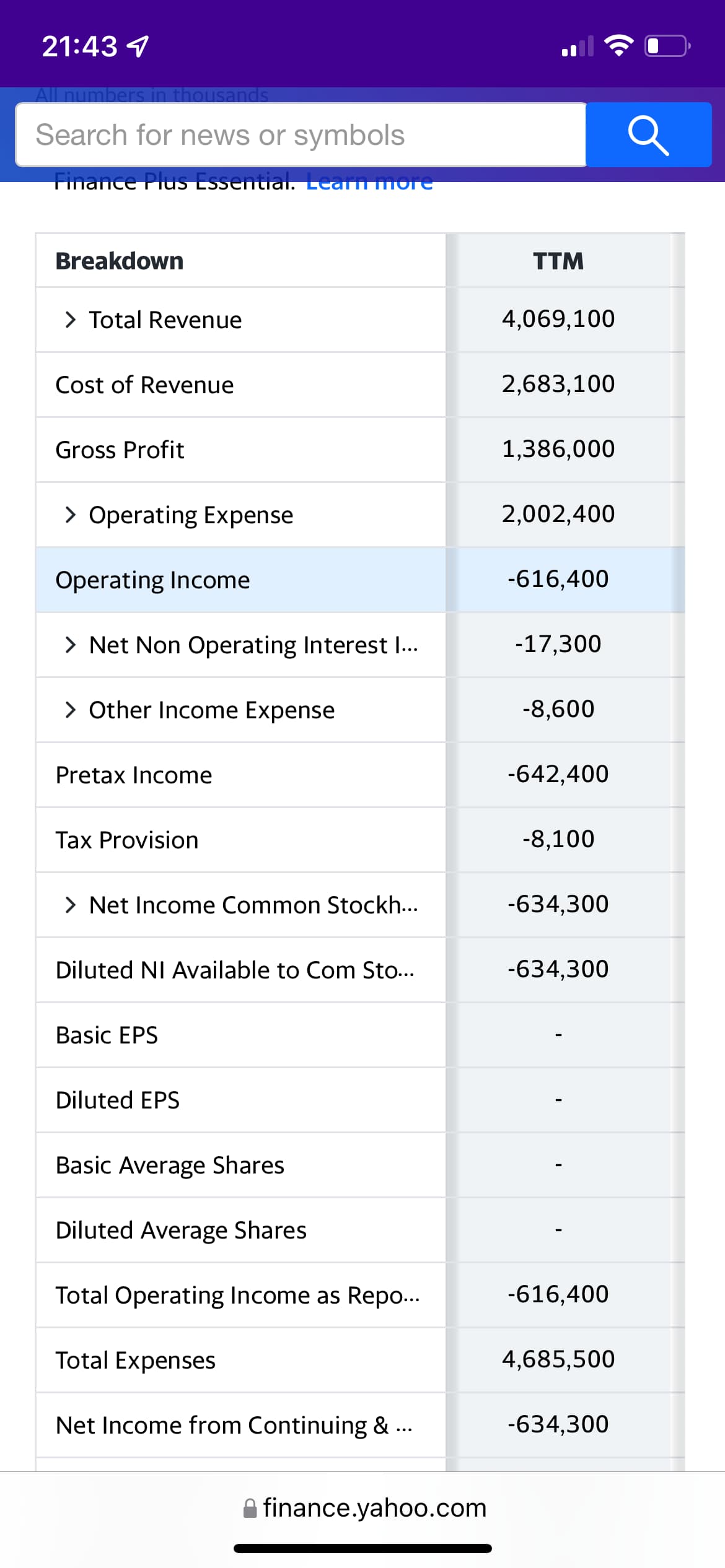

I think PTON got over it’s skis a little on anticipating future growth. Financials not looking good, and no growth on the imminent horizon to help dig them out. They need to go through some serious cost cutting. That opex number is…ah… a little high.

We’ll get a better sense of their financials - both where they are at and the extent of their cost cutting plans - on the 8th from their Q2 earnings release and conference call (Fiscal Year is July 1 - June 30). No doubt they will use this opportunity (stock tanking) to clean house without destroying the asset.

I’m always surprised by how many people know someone with Peloton products on this forum, I’m in the UK and have never known anyone that I know mention them at all. Admittedly I am not exactly the life and soul of the party but never once has anyone said they own one.

Out of 244 people I follow on Strava, I would say I see 2, maybe 3 people are using TR regularly in terms of uploading workouts. These users range from beginner to domestic pro’s. Obviously some people may have things set privately and I only know about 175-200 of those people personally or acquaintance from racing etc, the rest will be pro’s.

Zwift on the other hand seems way more popular, I would estimate at least 40-50 people regularly upload workouts, my feed is full of them, especially at this time of year.

I don’t think TR appeals to many people at all within my circle, Zwift on the other hand is more of a turn on and go (people also do workouts, group rides, races etc) whereas even though the user may want to improve, they don’t want a full on structure. The training phases on TR are too long and daunting and not sure people have the want or will to create a proper training plan, that is just not the market here at all in my experience.

I realise in the US and other countries the weather can be pretty extreme for 3-6 months of the year whereas in the UK we generally only get pockets of time where you can’t ride (on the road at least) so that always makes me wonder if TR is more geared to those people who know that they wont be riding outside for quite sometime so it makes it easier to stick with a longer plan.